Start saving and make the most of your money with competitive interest and other benefits.

Individual Retirement Accounts (IRAs)

Pay the future you, for all of your hard work.

An Individual Retirement Account (IRA) is a tax-advantaged retirement savings account.

Types of IRAs

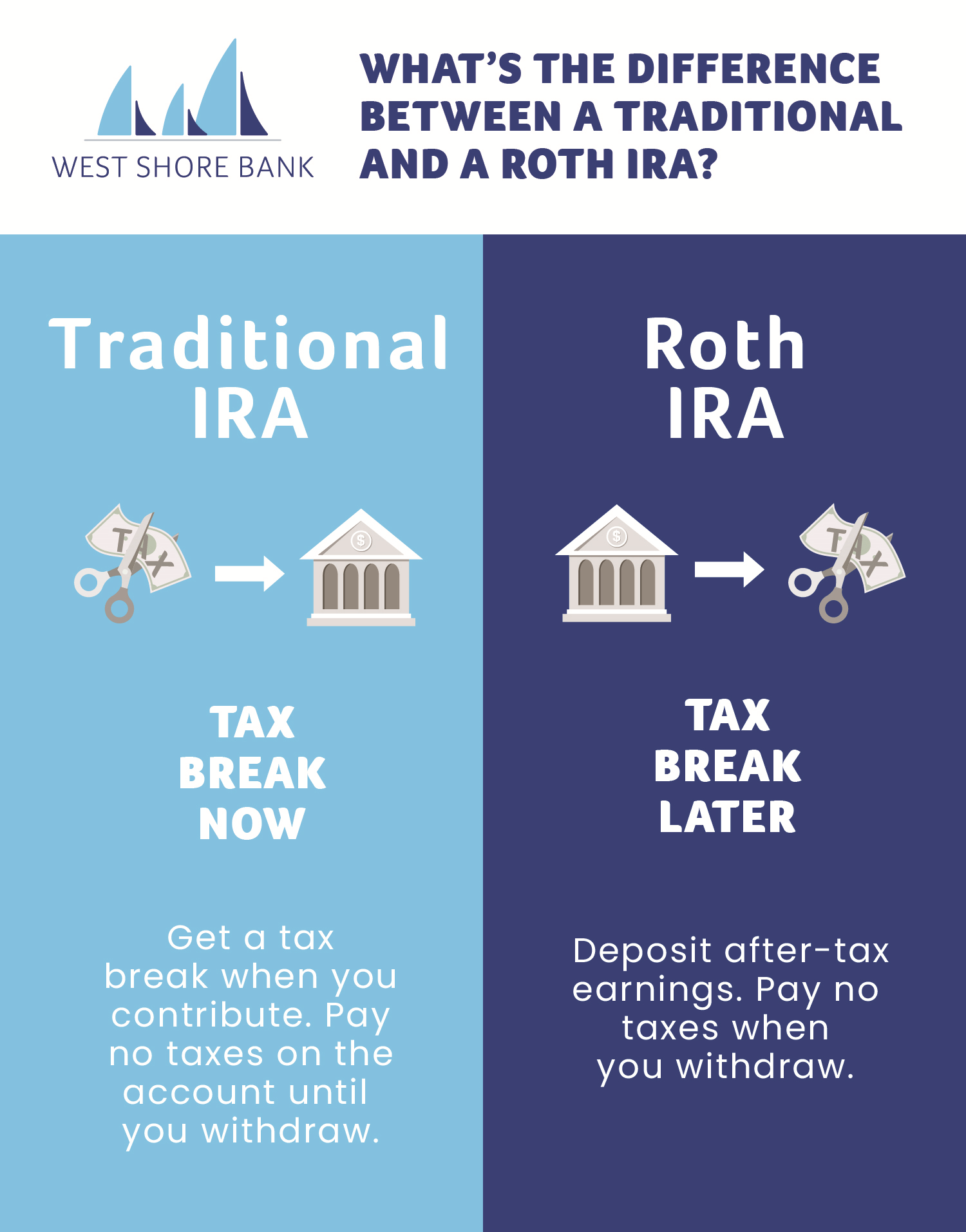

Traditional IRA

Contribute pre-tax dollars up to the annual limit. Earn interest on your IRA balance. Withdrawals in retirement are taxed.

Roth IRA

Make after-tax contributions up to the annual limit. Enjoy tax-free earnings and withdrawals.

Coverdell ESA

A type of education savings account that offers tax-free withdrawals for qualified education expenses. Earn interest on your funds to help pay for your child’s future education.

Traditional IRA vs. Roth IRA

Individual Retirement Accounts (IRAs) Rates

| Term | Fixed or Variable Rate | Minimum Balance* to Obtain APY | Interest Rate | APY (Annual Percentage Yield) |

|---|---|---|---|---|

| 12 Month IRA | Fixed | $500 | 2.00% | 2.02% |

| 24 Month IRA | Fixed | $500 | 2.50% | 2.52% |

| 36 Month IRA | Fixed | $500 | 2.50% | 2.52% |

| 48 Month IRA | Fixed | $500 | 2.50% | 2.52% |

*Daily Balance (the amount of principal in the account each day).

Withdrawals from certificates of deposit prior to maturity will be assessed early withdrawal penalties.

See Deposit Account Disclosure for more details.

How much can I contribute to my IRA each year?

The annual contribution limits for IRAs can vary based on the type of account. For 2026, individuals can contribute up to $7,500 to a Traditional or Roth IRA, with an additional $1,100. It's a great way to save for retirement while enjoying tax advantages.

What is the difference between a Traditional IRA and a Roth IRA?

A Traditional IRA allows you to contribute pre-tax dollars, which means you'll pay taxes on withdrawals during retirement. In contrast, a Roth IRA requires after-tax contributions, but your withdrawals, including earnings, are tax-free in retirement. Choosing the right option depends on your current tax situation and future expectations.

Can I withdraw funds from my IRA before retirement?

You can withdraw funds from your IRA before retirement, but keep in mind that early withdrawals may incur penalties and taxes. Traditional IRAs typically have a 10% penalty for early withdrawals before age 59½, while Roth IRAs allow you to withdraw contributions tax-free at any time. Always consult with a financial advisor for personalized guidance.

How do I open an IRA with West Shore Bank?

Opening an IRA with West Shore Bank is easy! You can start the process by visiting one of our local branches. Our friendly staff is here to help you understand your options and complete the necessary paperwork to get your retirement savings on track.

Is there a minimum balance required to open an IRA?

Yes, to open an IRA at West Shore Bank, a minimum balance of $500 is required. This ensures that you can start your retirement savings journey with a strong foundation.

What educational resources does West Shore Bank offer about IRAs?

West Shore Bank is committed to empowering our community with financial knowledge. We offer a variety of educational resources, including workshops, online articles, and one-on-one consultations with our financial advisors, to help you understand IRAs and make informed decisions for your retirement.

Can I roll over funds from another retirement account into an IRA?

Absolutely! You can roll over funds from other retirement accounts, such as 401(k)s or other IRAs, into a West Shore Bank IRA without incurring taxes or penalties. Our team can guide you through the rollover process to ensure it goes smoothly.

Are there any penalties for not withdrawing from my IRA?

While there are no penalties for not withdrawing from your IRA, Traditional IRAs require you to start taking minimum distributions starting at age 73. Failing to do so can result in penalties, so it's essential to plan accordingly with your financial advisor.