While the average pre-tax household income rose by 3.7% in 2021, according to the most recent Consumer Expenditures report from the Bureau of Labor Statistics, prices rose by 4.7% and average annual expenditures rose by 9.1%.

What these statistics tell us is that many individuals and families are trying to do more with less these days. If this is your situation, creating a budget is the best way to track your spending and make progress towards your financial goals. Whether you want to pay off debt, save for retirement, or work towards other financial goals--a budget will help you get there.

In this article, we’ll help new budgeters, as well as those who’ve tried before, create and stick with a budget.

Why Should You Create A Budget?

While a budget may feel constraining, if you do it right it should actually make you feel free.

Free to spend on something fun because you planned for it. Free from worry about whether you can “afford” something not. Free from guilt about what you spend money on.

Every time you get paid, money comes into your checking account. Then you have to make decisions. Some percentage of that money needs to go to bills and necessary expenses like groceries. But you get to decide what to do with the rest–put some of it towards your savings goals, keep some of it for discretionary spending.

A budget is for anyone who wants to keep track of their spending, not just people who are struggling financially. In fact, having a budgeting habit is a sign of good financial management.

In helping you track your spending and better align it with your goals and priorities, a budget can support you with:

- Avoiding overspending and falling into debt

- Saving for a home or other large purchases

- Saving for retirement

- Paying down debt

- Being prepared for emergencies

- Cutting unwanted spending

- Getting on the same financial page as your partner and improving communication around spending

How To Start a Budget

When you’re just getting started with budgeting, keep it simple. Start with your fixed monthly expenses such as a mortgage or rent payment, utility bills, phone, Internet, car loan, etc. Then you can move on to the expenses that recur every month but are also more flexible, such as groceries and entertainment.

How To Calculate Your Income and Expenses

- List and add your household’s monthly (take-home) income.

This includes paychecks from an employer, freelance or contractor income, investments, child support or alimony, retirement accounts, etc. include any pay from employment and other sources. Some people have very predictable income, while for others it may fluctuate from month to month. If you are in the latter camp, just make your best estimate. - List and add your fixed expenses.

This includes your housing payment (rent or mortgage); installment loan payments such as for a car, student, or personal loan; cellphone bill, water bill, cable/Internet, etc. - List your variable expenses.

Here’s where you budget for groceries, gas and electric, transportation costs, and any other necessities that fluctuate in cost. Again, make your best estimates and don’t worry if you end up a little over in one category or another. You can always draw from discretionary spending to make up the difference. - List your discretionary spending categories.

Everyone has different interests and hobbies. Some people love to travel; others go out to eat every weekend. You may love clothes, buying plants for your garden, or cycling. These are just some examples–write down what’s important to you. You may not have enough money left for all your discretionary categories, but you still have a choice in where to allocate your funds. - List your savings goals.

If you contribute to an employer-sponsored retirement account such as a 401(k), or a Health Savings Account (HSA), you don’t need to list these pre-tax distributions in your budget. But other savings goals, such as a college fund for your kids, an emergency fund, Christmas Club, vacation savings, or Individual Retirement Account (IRA) should be accounted for in your budget. It’s a good idea to schedule automatic recurring transfers on the days you get paid. Put your savings on auto-pilot so you don’t have to think about it.

Once you’re done making these lists, your budget needs to pass a simple math equation: Total Income-Total Spending. If your expenses exceed your income, you’ll need to cut back on discretionary spending or increase your income.

Want to calculate how long it will take to reach your savings goals or pay off a loan Check out our financial calculators. You can also use our home budget calculator to help you create your budget.

Determine Your Goals

Once you’ve created your first budget, keep your goals top of mind to help you stay on track. You may even be motivated to look for ways to reduce your discretionary spending, so that you can put that money into savings or paying off debt instead. Examples of goals include:

- Pay down debt

- Buy your first home or a vacation home

- Save for your child’s college education

- Save for your retirement

- Save for an emergency

- Save for your next vacation

- …or anything else that’s important to you!

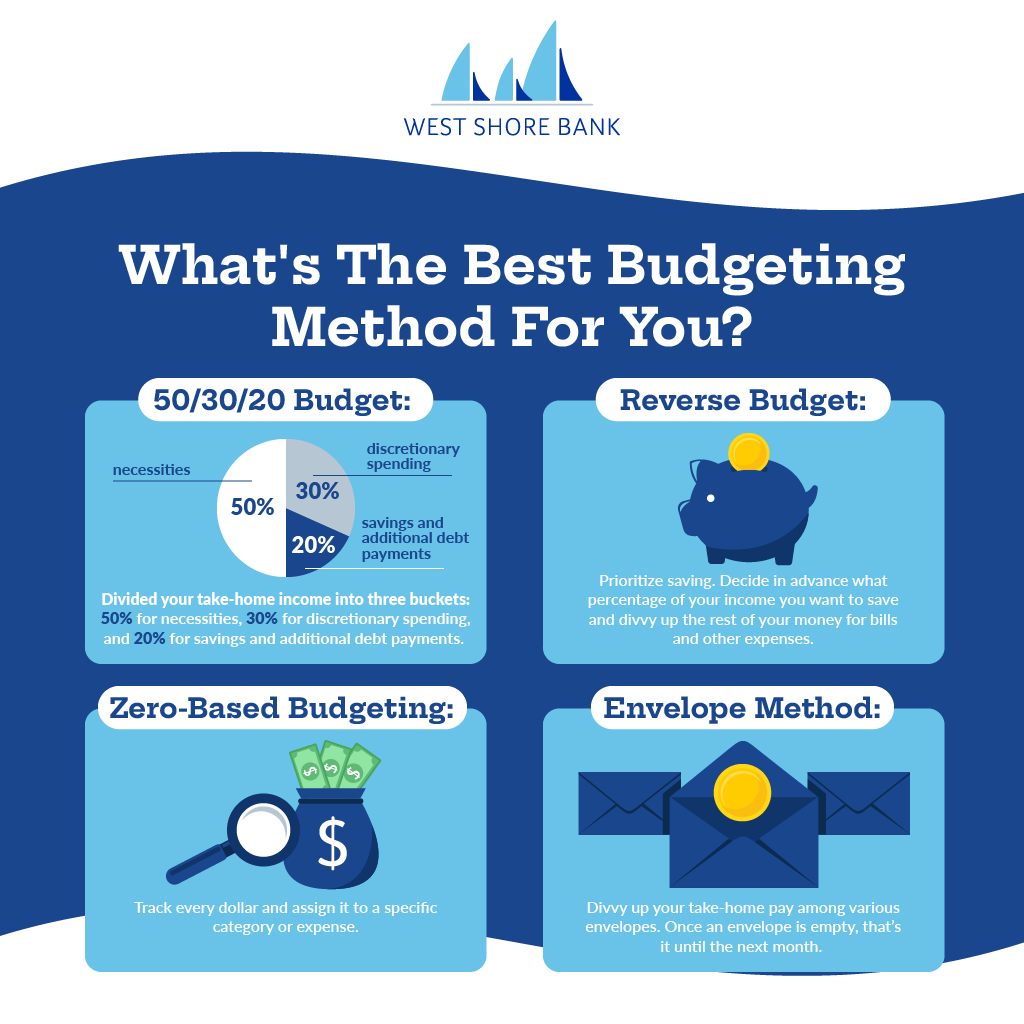

Find The Best Budgeting Method for You

Believe it or not, there is more than one approach to budgeting. Several approaches, in fact. You may need to try more than one before you find the one that works best for you. Here are some popular budgeting methods you can try out.

- 50/30/20 Budget: This approach divides your take-home income into three buckets: 50% for necessities, 30% for discretionary spending, and 20% for savings and additional debt payments. You can create your own variation of this budget, such as 60/20/20 or 70/20/10 to better fit your financial situation.

- Reverse Budget: Also known as the Pay Yourself First budget, this approach prioritizes saving. You decide in advance what percentage of your income you want to save, such as 10 or 20%, and put that into savings accounts before divvying up the rest of your money for bills and other expenses.

- Zero-Based Budgeting: For people who want to get down to the nitty gritty, this approach means tracking every dollar and assigning it to a specific category or expense.

- Envelope Method: You can do this type of budget with physical envelopes and cash, or in a digital version. Either way, you divvy up your take-home pay among the various envelopes (categories) and once an envelope is empty, that’s it until the start of the next month.

Testing Your Budget

Once you’ve selected a budget method, test it out for a month or two. If you find you’re not able to stick to the plan you created, adjust your budget. If that still isn’t working, try another method.

In addition to your budgeting method, use our MoneyTracker tool to help you stay on track with your budget, set financial goals and track spending. MoneyTracker is available through our digital banking platform.